- At a Glance: 2026 Cyprus Mortgage Key Metrics for Foreigners

- Critical First Step: Republic of Cyprus vs. North Cyprus Mortgages

- Mortgaging in the Republic of Cyprus (EU-Regulated)

- Financing in North Cyprus (Non-EU, Developer-Led)

- Who is Eligible for a Cyprus Mortgage in 2026?

- Eligibility Criteria for EU Citizens

- Eligibility Criteria for Non-EU Citizens (UK, US, Israel, etc.)

- Common Reasons for Mortgage Refusal

- Cyprus Mortgage Key Figures: Interest Rates & Loan Terms for 2026

- Interest Rates Breakdown: Variable vs. Fixed

- Loan-to-Value (LTV) and Down Payment Requirements

- Loan Duration & Maximum Loan Amounts

- Currency Risk Explained (EUR vs. Non-EUR Income)

- Estimate Your Monthly Mortgage Payments: 2026 Cyprus Calculator

- How to Get a Mortgage in Cyprus: The 7-Step Process for 2026

- Step 1: Initial Financial Assessment & Pre-Approval

- Step 2: Appointing a Lawyer & Finding a Property

- Step 3: Formal Mortgage Application & Document Submission

- Step 4: Bank’s Property Valuation

- Step 5: Obtaining Council of Ministers’ Permit (Non-EU Buyers)

- Step 6: Signing the Loan Agreement & Sales Contract

- Step 7: Transaction Completion & Title Deed Transfer

- Required Documents for a Cyprus Mortgage Application

- Personal Identification Documents

- Proof of Income & Employment

- Property-Related Documents

- Best Banks for a Property Mortgage in Cyprus: A 2026 Comparison

- The Full Cost: Understanding Fees Beyond the Loan

- One-Time Purchase Costs & Fees

- Stamp Duty

- Property Transfer Fees

- Legal Fees

- Mortgage-Related Costs

- Application & Arrangement Fees

- Valuation Fees

- Mortgage Registration Fees

- Ongoing Property Ownership Taxes

- Immovable Property Tax (IPT) & Local Authority Fees

- The Unique Advantage: Linking Your Mortgage to Cyprus Permanent Residency

- Oliver Bennett’s Insider Tips & 2026 Market Outlook

- 3 Costly Mistakes Foreign Buyers Make (And How to Avoid Them)

- 2026 Cyprus Property Market Forecast

- Outlook for Paphos, Limassol, Larnaca

- Strategic Choice: Off-Plan vs. Resale Properties for Financed Purchases

- Navigate the Cyprus Mortgage Process with Expert Guidance

- Frequently Asked Questions (FAQ)

As someone who has helped countless people make Cyprus their home, I’ve created this guide to walk you through the full process of securing a mortgage in Cyprus as a foreign buyer. It covers eligibility, current rates for 2026, required documents, bank comparisons, and the practical steps I’ve seen work time and again. Whether you are an EU citizen or a non-resident, the focus is on providing clear requirements and realistic timelines for buying property. My goal is to demystify the process and get you closer to your dream home under the sun.

Expert Introduction by Oliver Bennett (16-Year Cyprus Resident & Real Estate Specialist). This guide is updated for 2026.

At a Glance: 2026 Cyprus Mortgage Key Metrics for Foreigners

| Metric | Value |

| Avg. Interest Rate | 3.5% – 5.0% |

| Max LTV | 70% |

| Min. Down Payment | 30% |

| Typical Loan Duration | 15–25 years |

Key mortgage metrics for foreign buyers in Cyprus, 2026.

Critical First Step: Republic of Cyprus vs. North Cyprus Mortgages

A crucial first distinction I always make with clients is the stark difference in the mortgage framework between the Republic of Cyprus and North Cyprus. The choice you make here has significant legal and financial implications. The Republic operates under a transparent, EU-regulated banking system with internationally recognized title deeds and legally enforceable contracts, whereas North Cyprus primarily relies on developer financing, which carries a completely different set of legal risks.

Mortgaging in the Republic of Cyprus (EU-Regulated)

This is the secure and standard path. Banks here adhere to European Central Bank (ECB) regulations, which makes the financing process for your chosen property in Cyprus quite straightforward for approved buyers. More importantly, it provides you with stronger title deed security, which is the cornerstone of a safe property investment.

Financing in North Cyprus (Non-EU, Developer-Led)

Traditional bank mortgages are exceptionally rare in the North. Consequently, most purchases depend on developer-led payment plans. Because the legal framework and title deed system are not internationally recognized, buyers should exercise extreme caution. I strongly advise reviewing the dedicated section on Alternative Financing in North Cyprus before considering any transaction there.

Who is Eligible for a Cyprus Mortgage in 2026?

To get a mortgage in Cyprus, banks will meticulously assess your income stability, your global credit history, and the viability of the property itself. While the core principles are the same for everyone, the specific requirements differ slightly between EU and non-EU applicants.

Eligibility Criteria for EU Citizens

EU citizens applying for a Cyprus mortgage typically find the process smoother. You’ll need to provide solid proof of a steady income and a clean credit record from your home country. While being a Cyprus resident isn’t mandatory, having local employment or providing pension statements paid into a Cypriot bank account can significantly strengthen your application.

Eligibility Criteria for Non-EU Citizens (UK, US, Israel, etc.)

Non-EU buyers, including those from the UK, US, and Israel, face the same fundamental income tests but must also pass additional due diligence checks on the source of their funds. Banks are vigilant about anti-money laundering regulations. A minimum down payment of 30% is standard, and robust documentation is non-negotiable.

Common Reasons for Mortgage Refusal

From my experience, applications are most often declined for one of three reasons: insufficient or non-verifiable income, a poor credit history that appears on international checks, or issues with the chosen property itself—for example, if it fails the bank’s independent valuation or has legal encumbrances.

Cyprus Mortgage Key Figures: Interest Rates & Loan Terms for 2026

The rates for a Cyprus mortgage in 2026 generally hover between 3.5% and 5.0%. The final rate offered will depend on your personal financial profile, the loan amount, and whether you opt for a fixed or variable interest rate product.

Interest Rates Breakdown: Variable vs. Fixed

A variable rate is tied to the European Central Bank’s (ECB) base rate, so it can fluctuate, potentially lowering or increasing your monthly payments over the loan’s lifetime. A fixed rate provides payment certainty for an initial period (typically 3-10 years), which is excellent for budgeting, but it may start at a slightly higher rate than its variable counterpart.

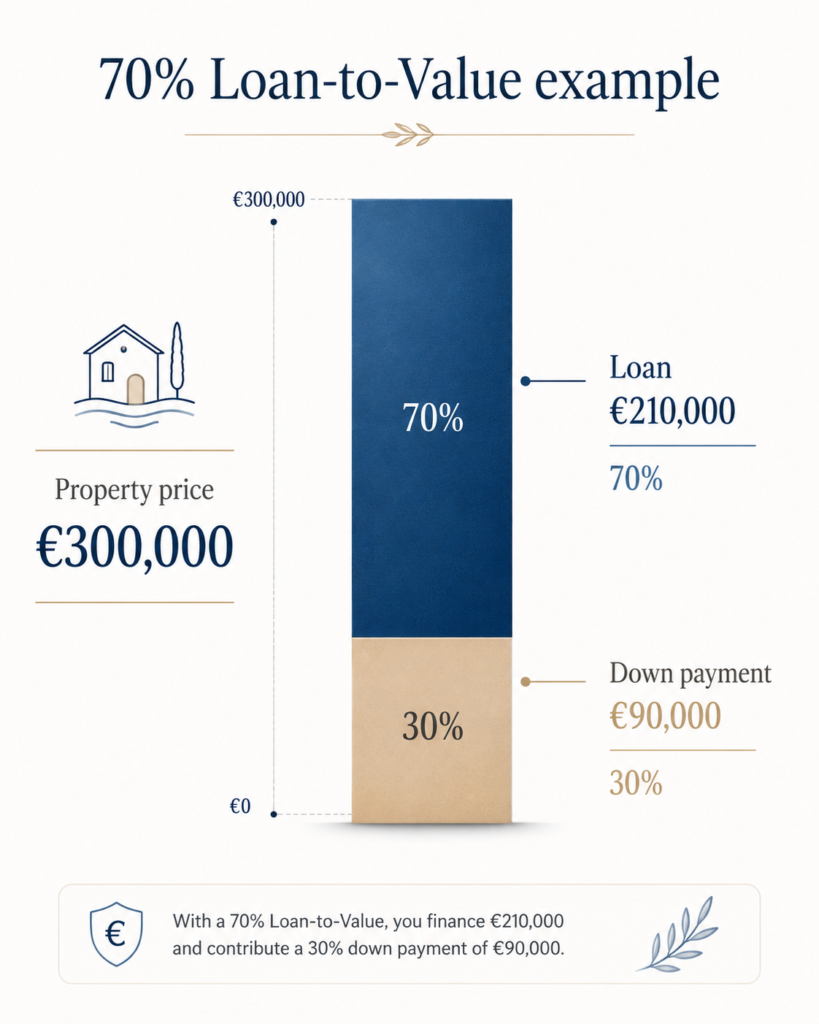

Loan-to-Value (LTV) and Down Payment Requirements

Banks in Cyprus are generally conservative with foreign buyers. They will typically offer financing for up to 70% of the property’s valuation price. This is known as the Loan-to-Value (LTV) ratio. Consequently, you must be prepared to provide at least 30% of the purchase price from your own personal funds as a down payment.

Loan Duration & Maximum Loan Amounts

Most mortgage agreements for foreign nationals span 15 to 25 years. The maximum loan amount a bank will offer is not just based on the property value, but is also determined by your ability to repay. The bank will calculate this based on your verified income and your age at the time of the loan’s maturity, which is typically capped at 65-70 years old.

Currency Risk Explained (EUR vs. Non-EUR Income)

This is a critical point for my clients from the UK, US, and other non-Eurozone countries. If your salary or primary income is in GBP or USD while your mortgage is in Euros, any adverse exchange rate swings can significantly increase your monthly repayment amount in your home currency. I often advise clients to consider hedging strategies or maintaining a Euro-based reserve account to mitigate this specific risk.

Estimate Your Monthly Mortgage Payments: 2026 Cyprus Calculator

Use our interactive calculator below to get a clearer picture of your potential monthly commitments. By inputting different property prices, down payment amounts, and interest rates, you can model various scenarios to find a budget that feels comfortable for you.

How to Get a Mortgage in Cyprus: The 7-Step Process for 2026

Navigating the mortgage process can seem daunting, but it’s a well-trodden path. The sequence below outlines the standard procedure based on current banking practices for 2026.

Step 1: Initial Financial Assessment & Pre-Approval

The first step is to obtain a pre-approval letter from a bank. This involves a preliminary review of your income and credit status. This letter is invaluable as it demonstrates to sellers that you are a serious buyer and defines your exact budget.

Step 2: Appointing a Lawyer & Finding a Property

With pre-approval in hand, you should appoint an independent local lawyer to represent your interests. They will conduct due diligence on any property you choose. Then comes the exciting part: finding your ideal home from the wide range of real estate for sale in Cyprus.

Step 3: Formal Mortgage Application & Document Submission

Once you’ve made an offer and it’s been accepted, you will submit your formal mortgage application along with a complete file of all the required supporting documents to your chosen bank. Accuracy and completeness here are key to avoiding delays.

Step 4: Bank’s Property Valuation

The bank will commission an independent surveyor to conduct a valuation of the property. This is to ensure the property’s market value is sufficient to secure the loan amount you have requested. This protects both you and the bank.

Step 5: Obtaining Council of Ministers’ Permit (Non-EU Buyers)

This is a mandatory step for all non-EU citizens buying property in Cyprus. Your lawyer will handle the application for the Council of Ministers’ permit to acquire immovable property. It’s largely a formality but is required before the sale can be legally registered.

Step 6: Signing the Loan Agreement & Sales Contract

Once the bank issues a formal letter of offer for the mortgage and your permit is approved, you will sign the final loan agreement. Typically, you will also sign the final contract of sale for the property around the same time.

Step 7: Transaction Completion & Title Deed Transfer

On the completion day, the bank disburses the loan funds directly to the seller. Your lawyer will then proceed with registering the property in your name at the Land Registry, and the title deeds will be transferred, securing your ownership.

Required Documents for a Cyprus Mortgage Application

To ensure a smooth application process, I advise my clients to prepare these documents well in advance. Delays are often caused by scrambling for paperwork at the last minute.

Personal Identification Documents

- A clear copy of your valid passport.

- A recent utility bill or official bank statement (no older than 3 months) as proof of your residential address.

Proof of Income & Employment

- Your last three to six months’ salary payslips.

- An official letter from your employer confirming your position, salary, and length of service.

- For self-employed applicants, two to three years of audited accounts and corresponding tax returns.

Property-Related Documents

- The signed reservation or sales agreement for the property.

- A copy of the property’s title deed or the original contract of sale if it’s a resale.

To keep track of everything, it helps to have a comprehensive checklist, which we cover frequently on our Cyprus expat blog.

Best Banks for a Property Mortgage in Cyprus: A 2026 Comparison

The table below provides a snapshot of the main banking institutions that are currently most active and friendly towards non-resident clients seeking a mortgage in Cyprus.

| Bank | Max LTV for Foreigners | Non-Resident Friendliness | Key Pro | Key Con |

| Bank of Cyprus | 70 % | High | Fast pre-approval process | Slightly higher arrangement fee |

| Hellenic Bank | 65 % | Medium | Competitive variable rates | Stricter income documentation requirements |

| Alpha Bank | 60 % | Medium | Flexible policies for pensioners | Lower LTV cap for most applicants |

Disclaimer: Rates and terms are indicative and subject to change based on market conditions and individual applicant profiles. Information last checked April 2026. For the most current and official offers, it is essential to consult the banks directly. See the official mortgage pages for the Bank of Cyprus and Hellenic Bank for more details.

The Full Cost: Understanding Fees Beyond the Loan

When budgeting for your property purchase, it’s crucial to look beyond the sticker price. In my experience, additional costs like stamp duty, legal fees, and transfer fees typically add 6–9% on top of the purchase price.

One-Time Purchase Costs & Fees

Stamp Duty

This is levied on the purchase contract and amounts to 0.15% on the first €170,860 and 0.20% on the value above that. It must be paid within 30 days of signing the contract.

Property Transfer Fees

These fees are payable to the Land Registry upon transfer of the title deeds. They are calculated on a tiered scale based on the property’s market value, ranging from 3% to 8%. Currently, a 50% discount is in effect, and they are waived for new properties subject to VAT.

Legal Fees

Hiring an independent lawyer is essential. Their fees for full transaction handling, including due diligence and contract reviews, typically amount to around 1% of the property purchase price, plus VAT.

Mortgage-Related Costs

Application & Arrangement Fees

Banks charge a one-time fee for processing and setting up your mortgage. This usually ranges from 0.5% to 1% of the total loan amount.

Valuation Fees

This covers the cost of the bank’s mandatory independent valuation of the property. Expect to pay between €300 and €600, depending on the property’s size and value.

Mortgage Registration Fees

A fee, typically around 0.1% of the secured loan amount, is charged by the Land Registry to register the bank’s mortgage lien against the property title.

Ongoing Property Ownership Taxes

Immovable Property Tax (IPT) & Local Authority Fees

A positive note for homeowners is that the national Immovable Property Tax (IPT) was abolished in 2017. However, you will still be responsible for modest annual local authority fees, which cover services like refuse collection, street lighting, and sewage.

The Unique Advantage: Linking Your Mortgage to Cyprus Permanent Residency

Here’s an angle many prospective buyers miss: a financed property purchase can be your ticket to the “Fast Track” Permanent Residency scheme. Even if you get a mortgage, you can still qualify, provided the total property value is at least €300,000 (plus VAT) and you can prove that the initial €200,000 (plus VAT) of equity was paid from funds transferred from abroad. This creates a powerful dual-purpose real estate investment in Cyprus. See our detailed Cyprus Permanent Residency guide for the full breakdown.

“Many of my clients don’t realize their property investment, facilitated by a mortgage, can simultaneously unlock a path to Cyprus Permanent Residency. It’s all about structuring the deal correctly from day one to meet both your housing and residency goals. It’s a fantastic two-for-one opportunity.”

— Oliver Bennett, Real Estate Specialist

Oliver Bennett’s Insider Tips & 2026 Market Outlook

After sixteen years of helping clients navigate this process, you start to see patterns—both the good and the bad. Here’s some advice straight from my personal experience.

3 Costly Mistakes Foreign Buyers Make (And How to Avoid Them)

- Underestimating currency fluctuations: Many buyers with non-euro income forget that a 10% swing in exchange rates can drastically change their monthly payments. Always budget for a buffer.

- Delaying a Cyprus Will: Your will from your home country may not be sufficient or easily enforceable here. Failing to draft a separate Cypriot will can create significant legal complications for your heirs.

- Choosing the first lawyer recommended: Often, a seller or agent will recommend a lawyer. Politely decline and find your own independent advisor. Your lawyer should work for you and only you.

2026 Cyprus Property Market Forecast

Outlook for Paphos, Limassol, Larnaca

From what I see on the ground, Paphos continues to be a magnet for first-time lifestyle buyers and retirees due to its affordability and relaxed atmosphere. Limassol maintains its position as the premium business and luxury hub, with steady rental demand from corporate tenants. Larnaca is the one to watch, offering a balanced mix of growth, family-friendly infrastructure, and new marina-front developments.

Strategic Choice: Off-Plan vs. Resale Properties for Financed Purchases

Securing a mortgage has different implications for off-plan versus resale properties. With off-plan units, you might face stage payments that need to be carefully aligned with mortgage drawdowns from the bank, which can be complex. In contrast, resale properties allow for an immediate valuation and can often lead to a faster and more straightforward mortgage completion.

Navigate the Cyprus Mortgage Process with Expert Guidance

If you’ve read through this guide and feel you would benefit from a second opinion on your numbers, help comparing current bank offers, or just want to chat about what life is really like here, please feel free to reach out. I’m always happy to help.

Frequently Asked Questions (FAQ)

How much deposit do I need for a mortgage in Cyprus as a foreigner?

As a general rule, you should expect to provide a minimum down payment of 30% of the property’s purchase price. Some banks may require up to 40% depending on your individual circumstances and the property type.

Can UK and US citizens get a mortgage in Cyprus after Brexit?

Yes, absolutely. UK, US, and other non-EU citizens can still secure a mortgage in Cyprus. You will simply be subject to the non-EU applicant criteria, which involves more detailed checks on your source of funds and requires a permit from the Council of Ministers.

What is the typical mortgage interest rate in Cyprus for 2026?

Current mortgage offers for 2026 typically have interest rates ranging from 3.5% to 5.0%. The final rate depends on the bank, the chosen product (variable or fixed), and your personal financial standing.

How long does the entire property buying and mortgage process take?

From having your offer accepted to receiving the keys and transferring the title deeds, a realistic timeframe is between three to five months. This allows for all legal checks, the mortgage approval process, and the non-EU permit application.

What are the main risks of taking a mortgage in a foreign currency?

The primary risk is currency fluctuation. If your income is in a non-Euro currency (like GBP or USD), and the Euro strengthens against it, your monthly mortgage payments will become more expensive in your home currency. This exchange rate risk should be a key part of your financial planning.